Full Report - Section 3

Devices, technology and ROI discipline

If regeneration is shaping what we deliver, technology is reshaping how we deliver it.

The next 12 months will not be defined by owning more devices. They will be defined by using them intelligently.

The device market: Still growing, but under scrutiny

Practitioners consistently predict continued growth in energy-based devices, particularly those supporting collagen stimulation, skin tightening and combination protocols

- Brands reinforce this, highlighting:

- Multi-functional platforms

- Radiofrequency and thermal technologies

- Reduced downtime protocols

- Precision-based energy delivery

- Companies overview

However, there is a crucial shift in tone.

Where previous years rewarded novelty, 2026 rewards efficiency and return on investment.

Companies explicitly state that performance alone is no longer enough. ROI, utilisation and commercial support are becoming decisive factors in purchasing decisions.

In short: capital expenditure is under a microscope.

Multi-platform over single-purpose

There is an increasing appetite for platforms capable of treating multiple indications.

The appeal is obvious:

- Higher room utilisation

- Cross-selling within consultation

- Reduced need for multiple machines

- More flexible treatment planning

Brands are emphasising multi-application platforms that combine fractional RF, IPL, vascular treatment, tightening and resurfacing in one system.

For clinics, the calculation becomes strategic:

Is this device a clinical add-on, or can it anchor a programme?

Intelligent energy and precision

Another notable shift is the emphasis on data-driven energy delivery.

- Industry voices describe:

- Real-time thermal modelling

- Ultrasound-integrated guidance

- AI-adjusted energy settings

- Fibre-guided precision in subdermal procedures

This aligns with the broader professionalisation trend.

Energy-based treatments are no longer viewed as operator art alone. They are moving toward reproducible, measurable endpoints.

That shift has two implications:

- Training must deepen.

- Documentation must improve.

Devices are becoming more sophisticated. Governance must follow.

The commercial discipline layer

Business service providers are clear: many clinics have historically scaled before stabilising systems

In 2026, device investment without workflow integration will expose weaknesses.

Before purchasing, clinics should model:

- Minimum monthly treatment targets

- Breakeven timeline

- Cross-referral impact

- Staffing and training requirements

- Marketing integration plan

If a device cannot integrate into a structured pathway, it risks becoming an expensive brochure prop.

Combination protocols as the profit engine

The strongest growth area for devices is not standalone treatments. It is integration into regenerative protocols.

Practitioners highlight combination approaches blending injectables with devices for subtle, layered outcomes.

Brands echo this, promoting structured pathways combining:

- Biostimulators

- Energy-based collagen stimulation

- Medical-grade skincare

- Maintenance scheduling

- Companies overview

From a revenue perspective, this is powerful.

Combination models:

- Increase average treatment value

- Extend patient journey length

- Reduce discount pressure

- Improve measurable outcomes

A device becomes more commercially viable when it supports a programme, not a one-off session.

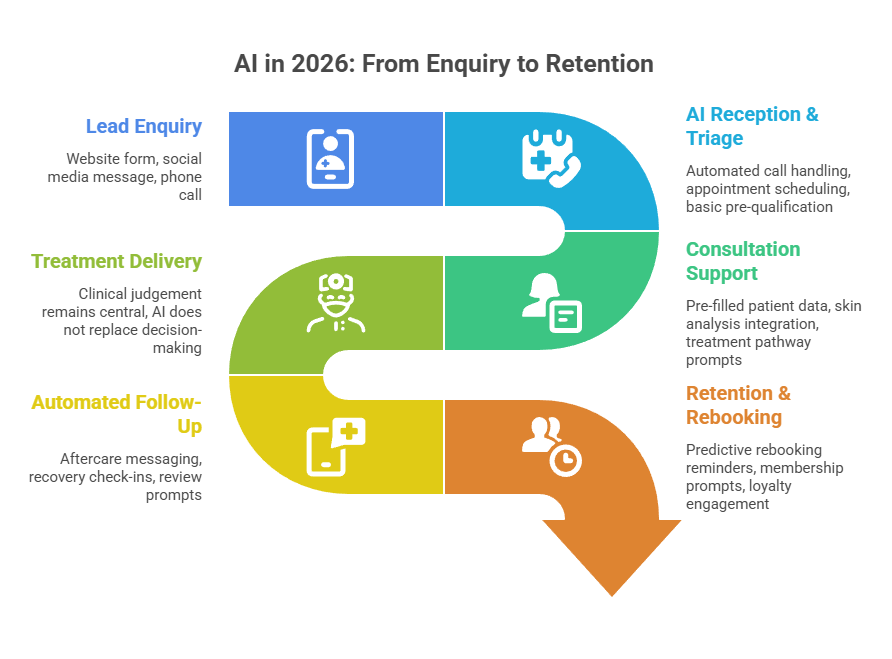

AI Integration: From tool to infrastructure

Technology is not limited to physical devices.

Artificial intelligence is now shaping:

- Booking optimisation

- Lead triage

- Automated follow-up

- CRM-driven retention

- Financial forecasting

- Business Services Trends

One striking insight from software providers is how much revenue clinics lose through missed calls and delayed response times

AI-powered reception tools, intelligent call handling and automated messaging are increasingly positioned as growth infrastructure rather than optional extras.

However, the warning is consistent: AI must support clinical judgement, not dilute it.

Technology enhances structure. It does not replace expertise.

Skin analysis: The quiet conversion driver

Another technology gaining importance is advanced skin analysis.

Industry contributors describe multi-spectral imaging, AI-driven diagnostics and integrated reporting systems becoming essential consultation tools

Why this matters:

- Removes subjectivity

- Standardises consultation quality

- Improves treatment acceptance

- Strengthens professional credibility

- Supports measurable progress tracking

Skin analysis devices are increasingly viewed as both clinical and commercial assets.

In a selective market, visual proof converts better than opinion.

The hidden risk: Over-expansion

There is an undercurrent of caution in the project files.

As competition intensifies, some clinics risk:

- Expanding device portfolios too quickly

- Adding services without system support

- Training teams superficially

- Relying on supplier marketing rather than internal positioning

The sector is maturing.

That maturity punishes overextension.

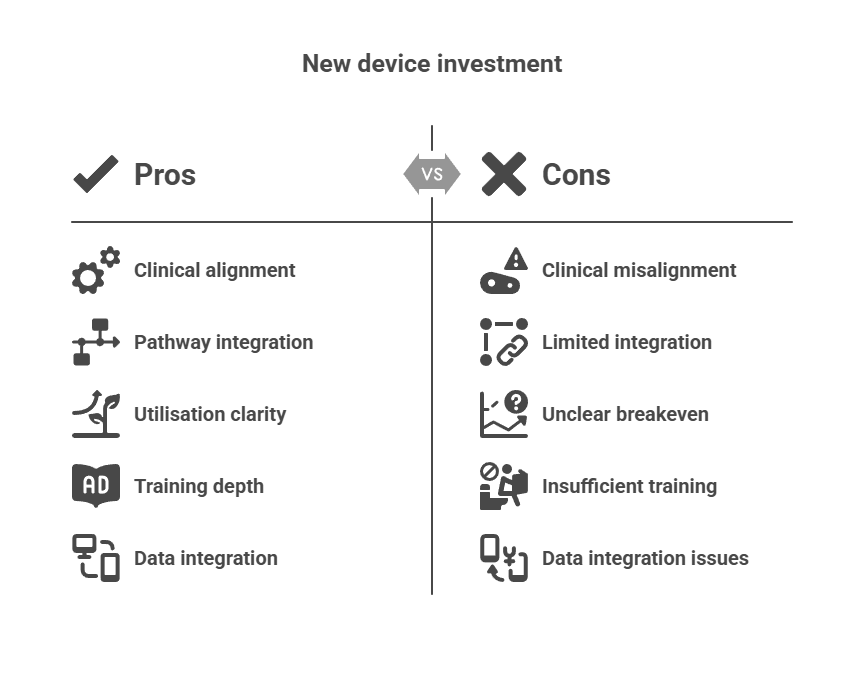

A practical device strategy for 2026

If you are reviewing technology this year, apply this decision filter:

- Clinical alignment: Does this device support your regenerative, longevity-led positioning?

- Pathway integration: Can it sit within a 6–12 month structured plan?

- Utilisation clarity: How many treatments per month are realistically achievable?

- Training depth: Is there documented competency progression?

- Data integration: Does it connect to CRM, reporting and measurable outcomes?

If any answer is vague, pause before committing.

The bigger pattern

The device landscape mirrors the wider market shift.

From: Impulse purchasing

To: Strategic infrastructure.

From: Treatment menu expansion

To: System integration.

From: Trend-led adoption

To: ROI-driven discipline.

Clinics that approach technology as part of an operational ecosystem will grow steadily.

Clinics that treat devices as headline features may struggle under margin pressure.